Connect with us on

Connect with us on

Overall: We maintain a cautiously optimistic view on Asian REITs, supported by falling interest rates across Asia ex-Japan, which enable lower financing costs and open the door for accretive acquisitions. Singapore exemplifies this trend, with Capitaland Ascendas acquiring assets at attractive cap rates using low-cost debt and equity raised at a premium to NAV.

Regional Highlights:

This article is an excerpt from the the white paper “Sustainability-Linked Insurance: Rewarding Climate Risk Adaptation” co-published by Link Asset Management, AXA and Marsh.

For decades, the real estate industry has viewed insurance as a necessary cost of doing business — a safeguard against unforeseen risks, but rarely a tool for creating value.

That paradigm is shifting.

Link Asset Management (Link) has introduced how real estate climate resilience efforts can be linked with insurance terms — a model that doesn’t just provide protection but actively rewards investment in climate adaptation measures.

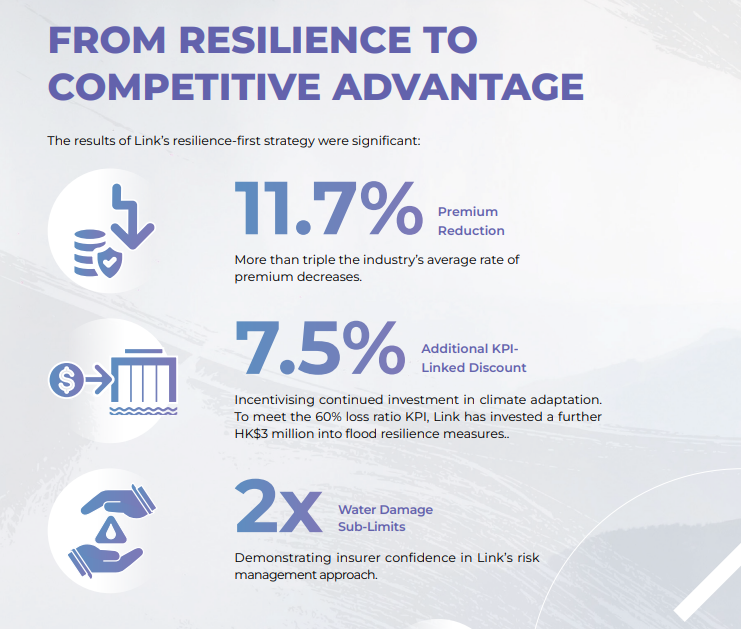

By quantifying climate risk and making targeted resilience investments, Link, through its insurance broker Marsh Hong Kong, secured an 11.7% reduction in property insurance premiums — significantly outperforming the industry’s ~3% average. Even more importantly, Link negotiated an additional 7.5% premium reduction tied to its loss ratio, creating a direct financial incentive to continue investing in long-term climate preparedness.

This case study isn’t just about one company’s success. Rather, it highlights a fundamental shift and real-time opportunity for real estate firms — and insurers — to align incentives and build climate resilience.

From Risk Awareness to Resilience in Action

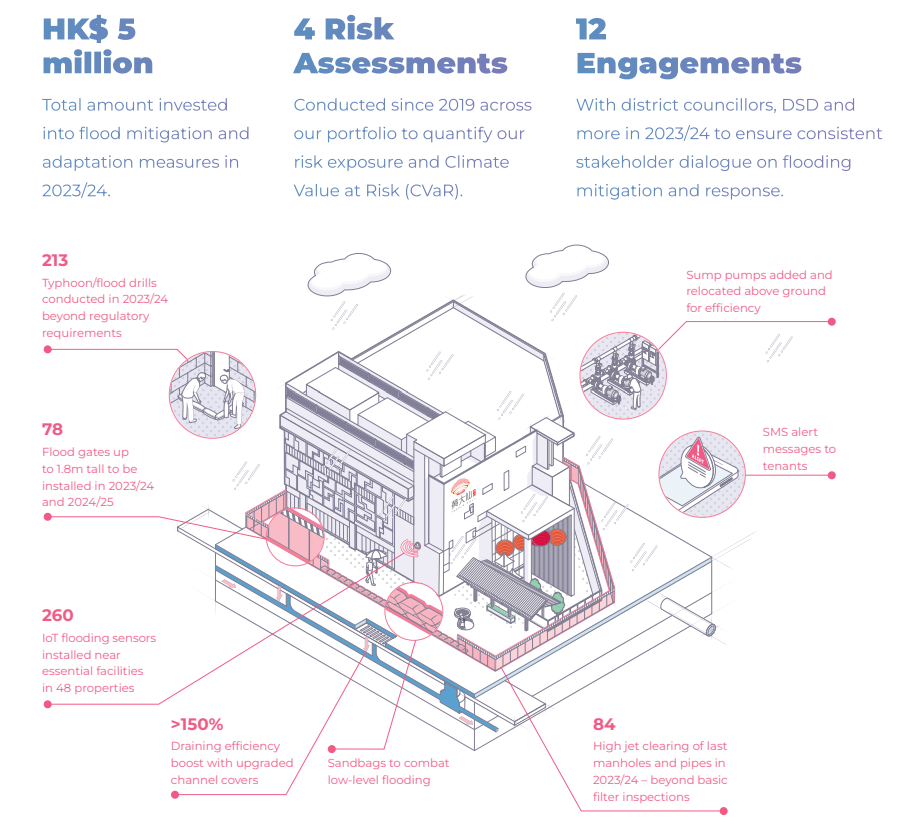

Extreme weather events are no longer an anomaly — they are an operational reality. In September 2023, Hong Kong experienced a “double whammy” of Super Typhoon Saola and record-breaking black rainstorms, causing widespread property damage. The conventional response across the real estate industry was reactive: filing claims, absorbing losses, and bracing for inevitable premium hikes.

Link chose a different approach. Rather than treating resilience as a cost, it saw an opportunity for investment — one that could be quantified, optimised, and ultimately rewarded.

Link reframed its relationship with insurers from a transactional one to a partnership in risk management:

By integrating risk identification, targeted mitigation, and transparent insurer engagement, Link transformed resilience from a defensive measure into a financial advantage.

The Resilience Framework: Six Pillars of Climate Adaptation

Building a resilience-linked insurance model requires a structured, data-backed approach. Link’s framework consists of six interconnected pillars:

Each of these pillars feeds into Link’s resilience-linked insurance structure, ensuring measurable risk reduction, operational stability, and long-term financial savings.

From Resilience to Competitive Advantage

The results of Link’s resilience-first strategy were significant:

By embedding climate resilience into its operational and financial strategy, Link has proven that climate adaptation isn’t just a defensive measure — it’s a value driver.

“We welcome the efforts made by Link REIT to make their assets more resilient and sustainable, and are pleased to show our support through promising insurance capacity and T&Cs. Extreme weather and climate risk are real issues for real estate and best tackled when all stakeholders work together.”

- Quoted by one insurer on an anonymous basis

What’s next?

Real estate is at a crossroads. Rising climate risks will continue to challenge traditional insurance models, but Link’s resilience-linked insurance structure offers a replicable blueprint for other asset owners.

The shift from reactive insurance to proactive risk management has begun — who will follow?

Read MoreEvolving work patterns in the post-pandemic era, employees’ demands for a better workplace experience, the large regional supply pipeline and high vacancy, and the urgent need to enhance older properties to maintain their competitiveness are just a few of the factors converging to drive a new era of office innovation in Asia Pacific.

Supported and enabled by the latest technology, landlords and investors are striving to enhance tenants’ experience at every stage of their employees’ day; from the commute, to the work environment, and to the leisure offering.

Our latest report explains how innovation can drive these improvements via three pillars of office innovation:

Singapore’s flexible workspace market has matured into a dynamic and diverse ecosystem, offering a broad range of solutions—from on-demand access for startups to fully managed suites for enterprises. This evolution reflects both the rising sophistication of occupier needs and the agility of operators in responding to them.

Today, with about 5% market penetration rate, the flex workspace market features a healthy mix of brand positions, ranging from premium hospitality-driven environments to value-oriented, efficiency-focused models. Our findings show that the top 10 brands (by market size) now command 80% of the market, with varied pricing and positioning offerings to meet the needs of businesses across all sizes and sectors. This ensures that companies can find workspaces aligned with their identity, culture, and operational goals.

Notably, flex space is increasingly integrated into asset strategies, with landlords and operators collaborating to enhance both building value and tenant experience. As the market continues to evolve, innovation and adaptability will be key to shaping the future of work. This report further explores what occupiers seek and how landlords and operators can continue to strengthen the value proposition of flexible workplaces in Singapore.

Download the Report Read More